{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Name of QuantLet: JumpDetectR

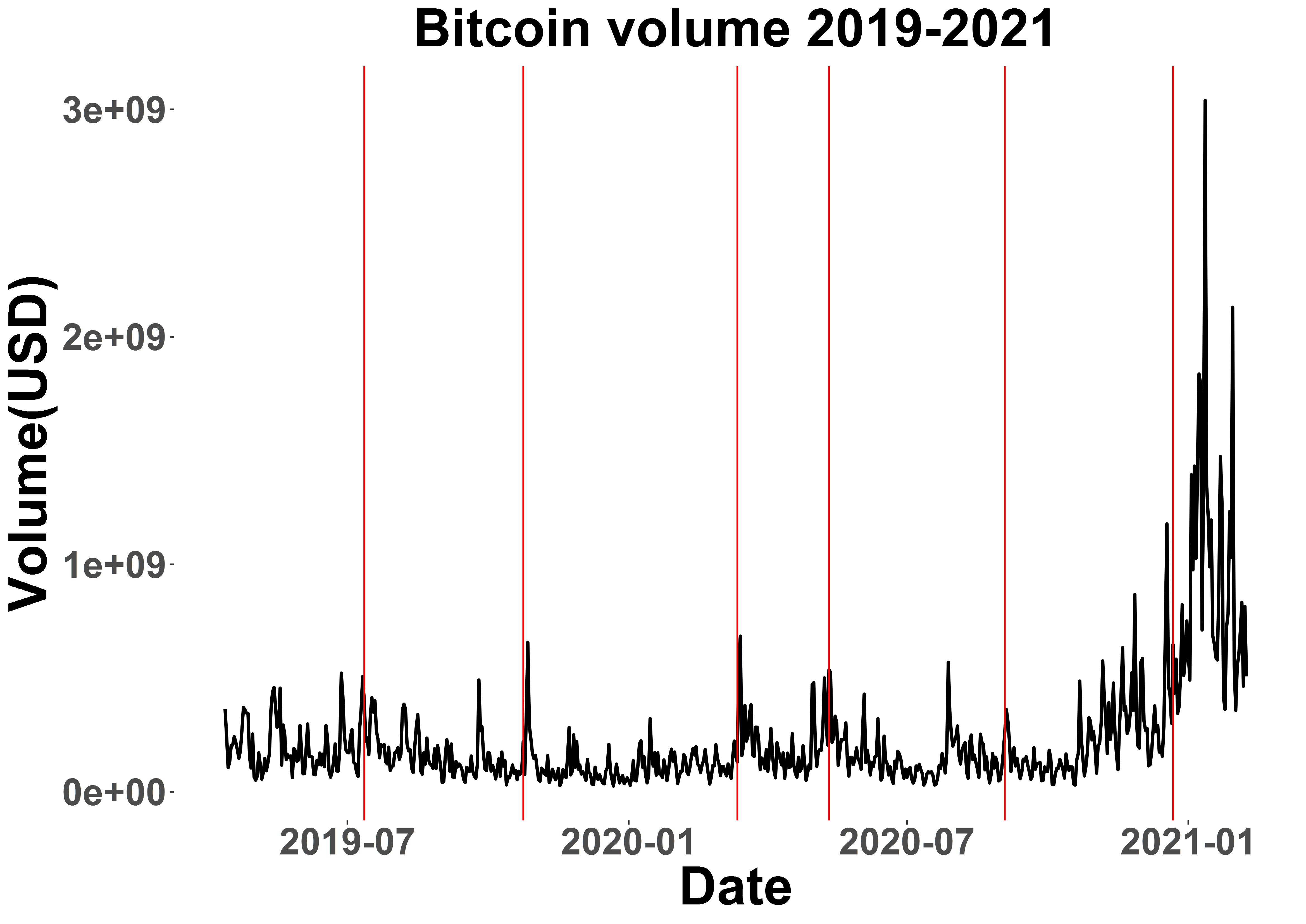

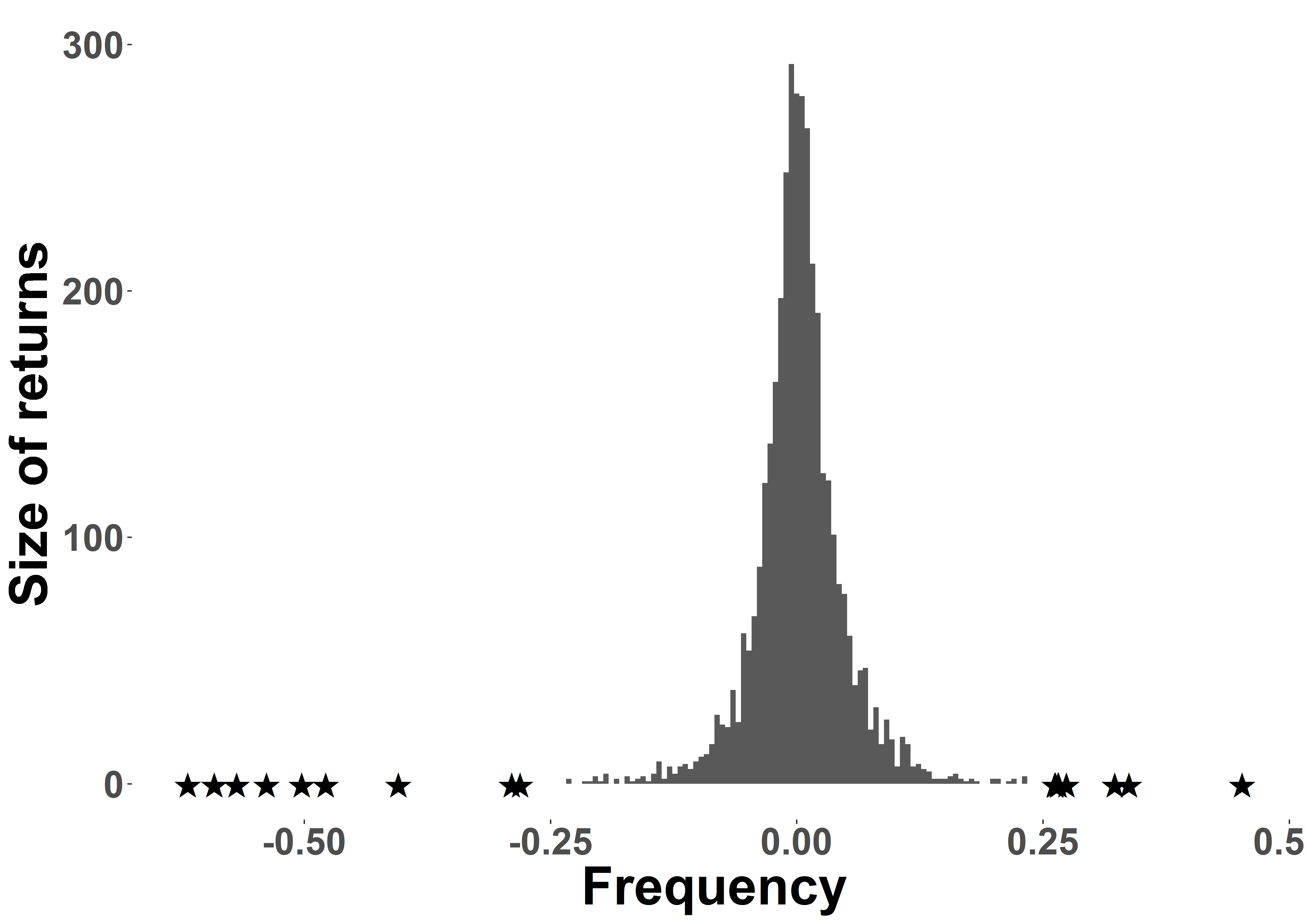

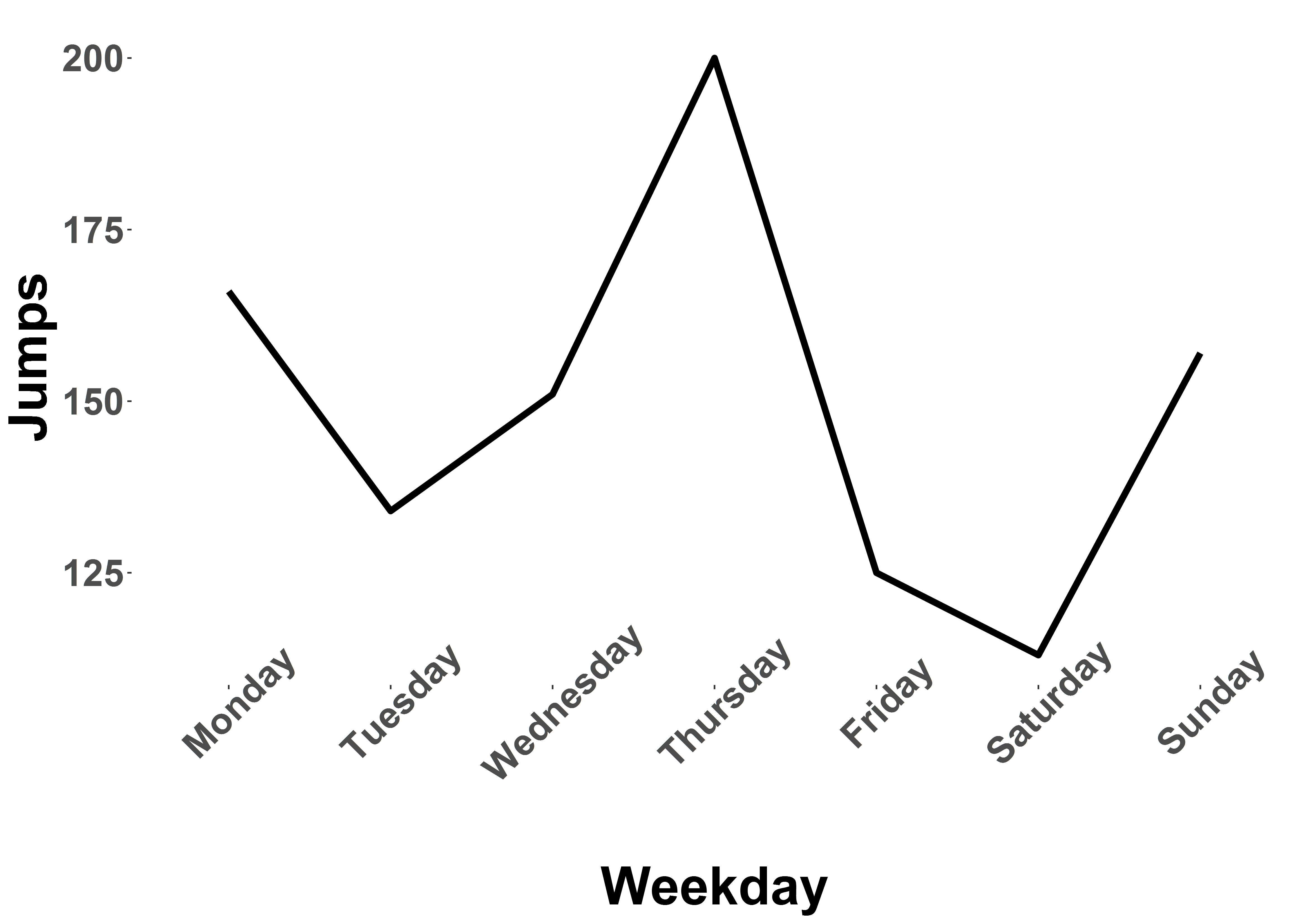

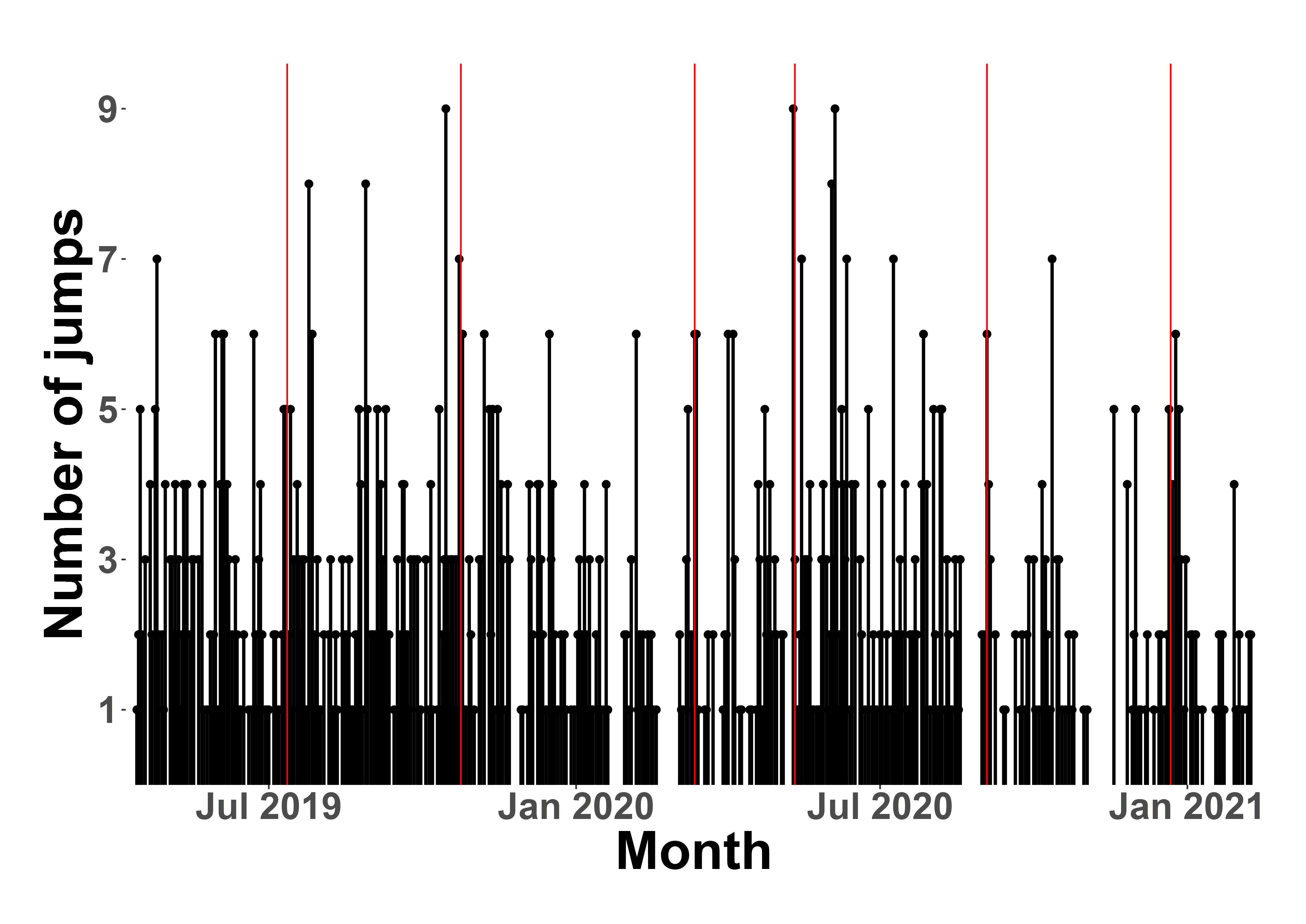

Published in: To be published as "Jump dynamics in high frequency crypto markets

Description: Scalable implementation of Lee / Mykland (2012) and Ait-Sahalia / Jacod / Li (2012) Jump tests for noisy high frequency data

Keywords: Jumps, jump test, high frequency, time series, Ait-Sahalia, Jacod, Lee, Mykland, stochastic processes, cryptocurrencies, cryptocurrency, crypto, spectrogram, microstructure, market microstructure noise, contagion, shocks

See also: Lee, S.S. and Mykland, P.A. (2012) Jumps in Equilibrium Prices and Market Microstructure Noise; Ait-Sahalia, Y. and Jacod, J., Jia Li (2012) Testing for jumps in noisy high frequency data

Authors: Danial Florian Saef, Odett Nagy

Submitted: May 7 2021 by Danial Saef